The US government is currently in the process of changing the federal tax framework. There is a lot of discussion about the content of these changes, how it will affect business environments, personal finances, and government departments. The bottom line is that taxation is a complex issue and that nobody will know its exact impacts until it is actually implemented and in place for some time. For example, the new tax bill is will reduce corporate taxes in an attempt to increase economic growth. What is unknown is how companies will employ this additional revenue. Will they reinvest it in US economy or just pay dividends to shareholders of which a significant portion of them are outside the US? Our opinion is that tax regulation, as well as many other complex government regulations should be implemented based on Adaptive Project Management principles. Here are the five basic principles of adaptive project management:

Principle 1: Using actual project data in combination with original assumptions.

In project management during project execution new information and results may become available. This new information can be used to adjust the original model assumptions and make necessary corrections. In project management the model is “project schedule”. In the example of taxation the model is a framework, which can always be corrected based on actual results.

Principle 2: Minimizing the cost of decision reversions.

Each time a decision is changed it can have a cost associated with it. The cost may not only be strictly monetary. For example, if some group of organizations receive a tax break and then it needs to be reversed, it will lead to loss aversion. Loss Aversion is the tendency of decision-makers to prefer avoiding losses versus acquiring gains. This may lead to a significant political cost because these organizations will push to preserve reduced tax levels. However; if tax is originally reduced insignificantly, cost of reversal can be less.

Principle 3: Making smaller sequential decisions.

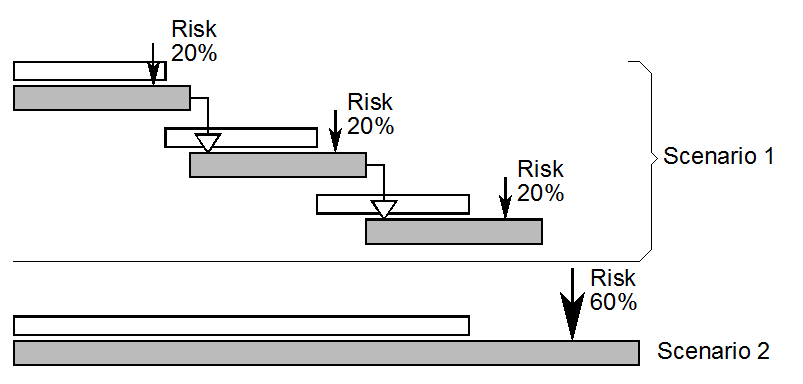

Many projects are completed earlier or cost less if they are done iteratively with many smaller tasks rather than afew larger tasks. The example below illustrates this point. What will be completed earlier: three sequential tasks or one task 3 times longer affected by the risk “Restart task” with 20% probability?

It happens to be that scenario 1 will take on average 25% less time than scenario 2. Similar results can be demonstrated for cost, one large or few smaller expenditures. In the case of tax legislation, a number of small updates to tax policy will lead to less potential loses and less policy reversions than one large change.

Principle 4: Supporting creative business environments.

If during a the course of a project you receive new information, you should be able to use this information to steer the project in a better or more optimal direction. At the same time, you do not want to create chaos by making frequent u-turns as a response to small requests or a changing business environment.

Principle 5: Early identification and fixing of issues.

The longer we continue with an incorrect course of action, the more difficult it will be to reverse the course of action. This is related to the so called “sunk cost effect” when people make a choice considering the cost that has already been incurred and cannot be recovered. For example, when any earlier issues with tax policy are unidentified then any cost associated with fixing them will be less.